Finance Act 2023 Nullified: Impact on Salaries, Fuel, and Other Taxable Items

The legislation, designed to introduce various tax initiatives to boost revenue and tackle economic issues, has been declared invalid.

This invalidation hinders the enforcement of key tax policies and casts doubts on the government’s future fiscal plans.

In this discussion, we delve into the significant tax measures impacted by the court’s ruling and their possible consequences.

The Finance Act 2023 introduced several significant tax measures in Kenya, effective from various dates, primarily aimed at increasing revenue and expanding the tax base. Here are the key highlights:

Value Added Tax (VAT) and Levies

VAT on petroleum products, excluding liquefied petroleum gas, was increased from 8% to 16%, significantly impacting fuel prices.

The Finance Act 2023 zero-rated VAT for

- Liquefied petroleum gas (LPG)

- Supply of locally assembled and manufactured mobile phones;

- The supply of motorcycles of tariff heading 8711.60.00;

- The supply of electric bicycles.

- The supply of solar and lithium-ion batteries;

- The supply of electric buses of tariff heading 87.02;

- Inputs or raw materials locally purchased or imported for the manufacture of animal feeds;

- Bioethanol vapor (BEV) stoves are classified under HS Code 12.00 (cooking appliances and plate warmers for liquid fuel)

- All tea and coffee are locally purchased for value addition before exportation subject to approval by the Commissioner General.

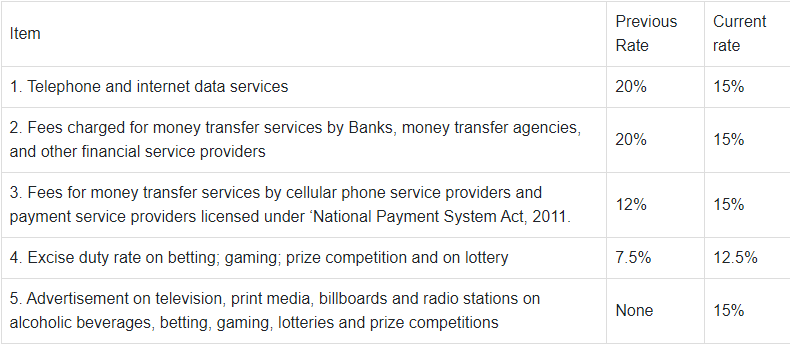

Excise Duty

The Finance Act 2023 proposed the excise duty as follows:

The following items were also brought under the tax net:

A mandatory housing levy was introduced, requiring both employers and employees to contribute 1.5% of the employee’s gross salary to the National Housing Development Fund.

However, the housing levy was later anchored on the Affordable Housing Act, 2024 which means it will not be affected.

Income Tax Changes

The Act introduced new income tax rates for individuals. A rate of 32.5% was applied to monthly income between Sh500,000 and Sh800,000, while a 35% rate was set for income exceeding Sh800,000.

Travel allowances provided to employees for official duties were exempted from taxation, provided they adhered to the approved standard mileage rate.

Club entrance and subscription fees paid by employers on behalf of employees were classified as taxable benefits, thereby subjecting them to income tax.

A relief of 15% on contributions to post-retirement medical funds was introduced, capped at Sh60,000 per annum, effective January 1, 2024.

Digital Content Monetisation

Digital content monetization was subjected to withholding tax at the rate of 5% for residents and 20% for non-residents without a permanent establishment in Kenya.

Compliance and Administrative Changes

To enhance tax compliance, expenditures or losses would not be deductible unless invoices were generated through the electronic tax invoicing management system (e-TIMS), effective January 1, 2024.

The Act mandated that withholding tax be remitted to the Kenya Revenue Authority within five days of payment, tightening the timeline for tax compliance.

Corporate and Other Taxes

The Act imposed a 15% tax on repatriated income for non-residents with a permanent establishment in Kenya.

Additionally, the Corporate Income Tax (CIT) rate was reduced from 37.5% to 30%, effective January 1, 2024.

The upper threshold for turnover tax was reduced from Sh50 million to Sh25 million, with an increase in the tax rate from 1% to 3%.

A new tax of 3% was introduced on income derived from the transfer or exchange of digital assets, effective September 1, 2023.

Withholding Tax

Withholding tax on payments for use of immovable property was reduced from 10% to 7.5%.

The Finance Act 2023 introduced withholding tax on the following payments:

- Sales promotion, marketing, and advertising services for residents -5%

- Digital content monetization to residents at 5% and 20% to non-residents;

- Rental income received on behalf of the owner of a premises provided that only a person appointed by the Commissioner in writing shall deduct tax about rental income.

Advance tax

The advance tax was reviewed as follows

- Vans, pickup trucks, prime movers, trailers, and lorries – Sh2,500 per tonne of load capacity per year or Sh5,000 per year whichever is higher.

- Saloons, station wagons, mini-buses, buses, and coaches – Sh100 per passenger capacity per month or Sh5,000 per year whichever is higher.

Rental Income

Residential Rental income tax (MRI) rate was reduced from 10% to 7.5%.

Mortgage interest claims

Individuals were allowed to claim mortgage interest expense to a maximum of Sh300,000 per year incurred on money borrowed from a cooperative society.

The act introduced a tax on the income derived from the transfer or exchange of digital assets (such as cryptocurrency transactions) at a rate of 3%.

The nullification of the Finance Act, 2023 by the Court of Appeal has rendered these measures void, leading to significant uncertainty in the tax landscape.

The government had aimed to enhance revenue collection and improve fiscal policy through these measures.

However, the annulment disrupts the implementation of these taxes, potentially impacting government revenue and fiscal stability.

In the absence of an appeal, the government will have to revert to using the Finance Act 2022.

Finance Act 2023 Nullified: Impact on Salaries, Fuel, and Other Taxable Items